3.25.2026

Granola Has Officially Become a Unicorn

Today, Granola announced the close of a $125 million Series C financing, led by Index Ventures with participation from Kleiner Perkins, at a $1.5 billion valuation. Since inception three years ago (and public launch just one and a half years ago), the company has achieved unicorn status at a remarkable pace.

We were among the very first investors to invest in Chris and Sam, all the way back in 2023. Now, with Granola billboards strewn about major markets and basically everyone in the tech world using “Granola” as a verb, that bet seems fairly obvious. The decision to invest is made all the more obvious by the current positioning of Granola: a mission critical contextual layer that will undoubtedly power a personalized agentic future.

At the time, however, investing in Granola was actually a contrarian decision.

The Case Against

Circa 2022/2023, there was no shortage of first-generation AI notetakers. It was an eyeroll-worthy space, with Otter, Fireflies, and Fathom all holding significant market share in a category considered by many VCs to be a commodity. And that didn’t account for the bigger platforms.

It was clear that the incumbents, who had been powering work/meetings for many years, and who had gone through a compressed period of improving those systems during COVID, would absolutely build AI-powered note takers as features within their existing products.

In other words, Granola would be competing against a simple button or toggle (or, in the most nightmarish version of this, a default setting) inside Zoom, Meet, and Teams.

A war on two fronts: the AI notetakers with a headstart and the incumbent platforms with virtually unlimited distribution.

Beyond competition, a wider conversation was afoot among venture types. The Great Wrapper Debate of 2023, which actually wasn’t a debate so much as an instantly and widely adopted hot take, had many VCs worried about defensibility.

“It’s pretty thin.”

“It’s just a wrapper for GPT-4.”

The prevailing opinion, at that time, was that the cost of training and compute would create a compounding moat where all the value would accrue to the models, and the scraps (highly taxed) would be allotted to the thousands of applications that sat atop those models.

We know now, and at Betaworks we knew even then, that the commoditization of the foundation models, with relentless open source competition both domestically and abroad, would change that equation.

Back when we invested, Granola was undoubtedly perceived as a thin wrapper. We, too, used those very words when discussing the opportunity in IC. And it was among other demerits, such as the GTM strategy.

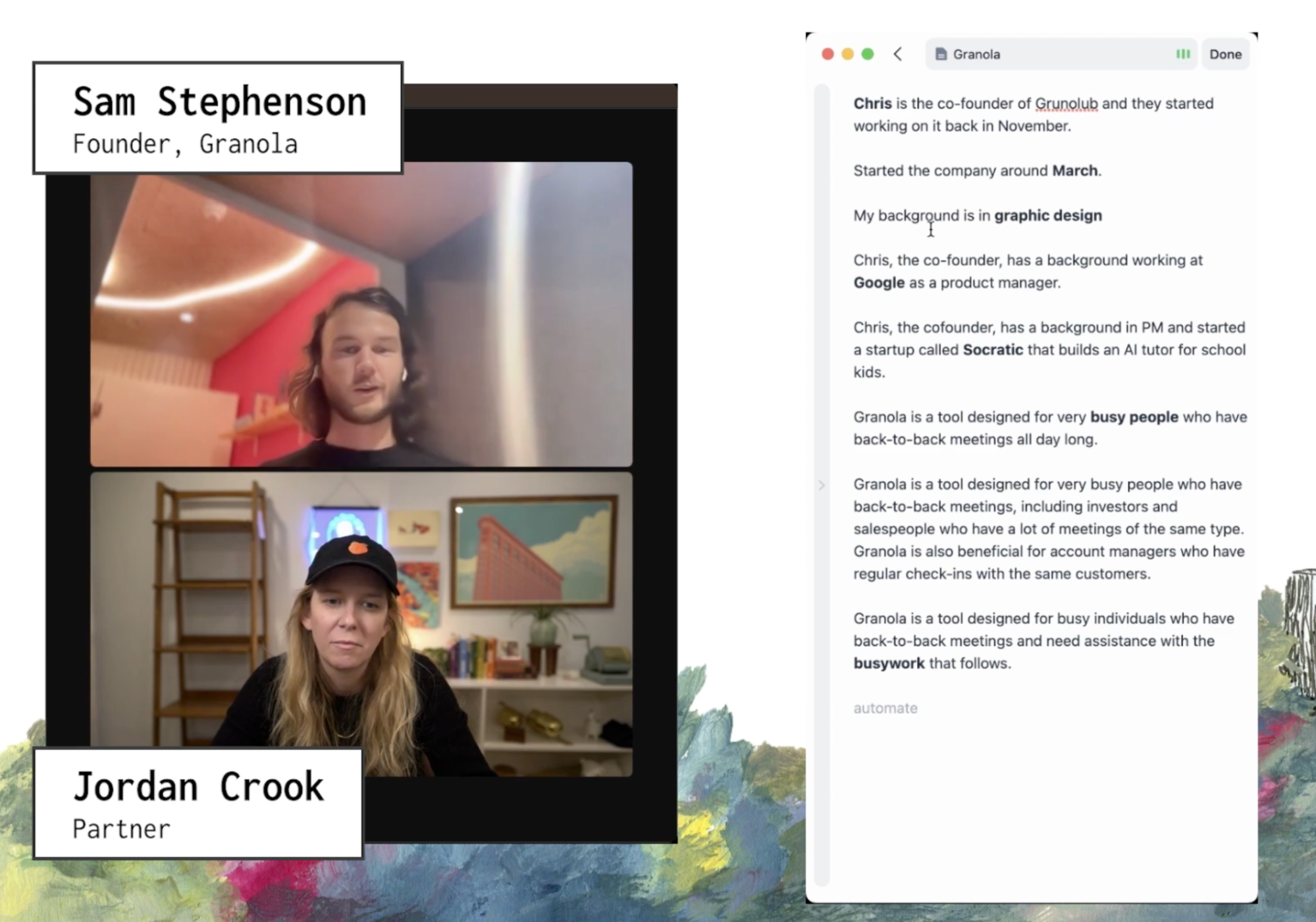

Chris and Sam were very aware of the breadth of this type of horizontal tool, and its value across a wide variety of users/professions. However, they were flirting with the idea of starting with VCs, who are a great representative of the ICP as people who have many back to back meetings that are similar yet distinct.

VCs are a notoriously shitty wedge and most investors see that as a pink flag, at the least. They’re famously disparate in their workflows, and tend to be a small market that rarely bleeds into anything bigger.

This ended up being a perfect starting place for this product, and it served multiple purposes for the company, including providing the team with an excess of (highly opinionated) product feedback and validation, as well as generating quite a bit of investor buzz. Those benefits weren’t obvious at the time.

The Case For

Betaworks invested in Chris Pedregal when he built Socratic. He was an impressive product builder, had attracted some 10+ million MAUs to the tutoring product, won App of the Year in 2017, and had an exit under his belt. The exit was solid, but not great. This is important. It implies that there was enough success to understand the playbook for product validation but not so much success to adequately remove the chip from Chris’ shoulder.

Sam, in many respects, was the perfect counterpart to Chris, an engineer with spectacular design chops and experience building productivity front-ends that were beloved by their users.

In other words, the team was highly investible and a known entity to the Betaworks team. We also liked the contrarian product insight.

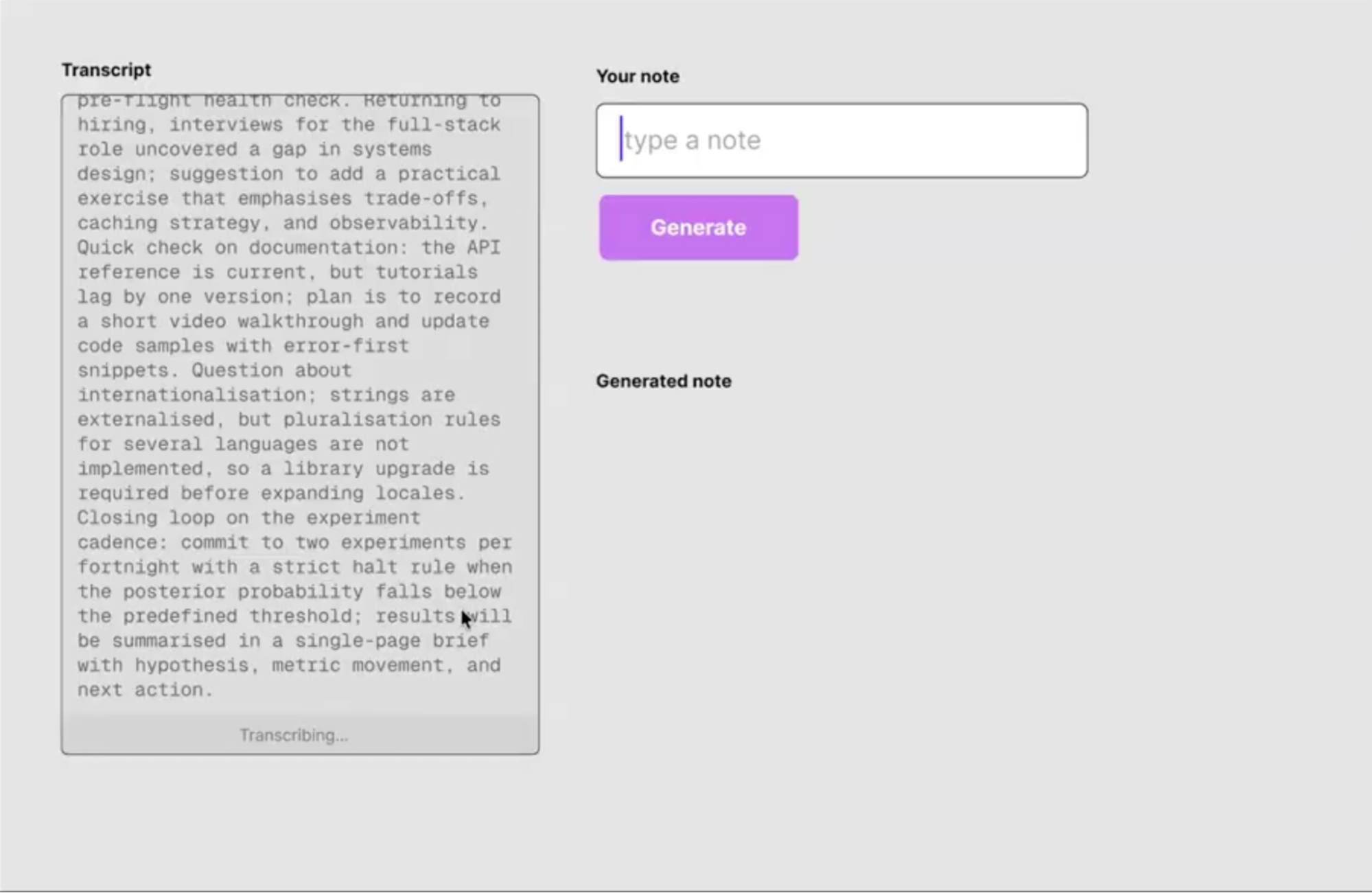

The prevailing wisdom in note-taking at the time was passive usage – a bot would join the meeting, transcribe, summarize, and deliver those notes to your inbox, etc. This was in complete opposition to Chris and Sam’s belief system about how LLMs would change the future of work. I can’t count the number of times I heard Chris say, “Writing is thinking.”

Much of the obsession for the Granola team, back then, was how to interact with meeting notes in real-time. In fact, the core feature that was pitched to us (and that I fell in love with and that I have pledged I would pay for should it be resurrected) was a tab button that would expand some trigger word into the complete transcript around that word.

Despite the fact that it’s no longer a part of the product, and that post-meeting activities are much more central to Granola’s value prop and road map, the concept of real-time meeting notes was highly resonant for me.

As a former journalist, the most critical skill that I developed was to ‘listen’. It’s easy, during an interview, to zone out when someone’s answering and focus on your next question. This is a mistake. The best interviewers listen and respond. Granola was building for that level of depth, exploration, curiosity, and human-powered thought.

But beyond the contrarian product direction and killer team, the timing of this product in conjunction with the thoughtful design had us particularly excited.

We spent quite some time discussing what would have to be true in order for Granola to be a billion dollar business. There were a few, all of which felt realistic and achievable by such a talented team.

The first was that Granola would need to have an “AI native” interface that leaned toward platform agnosticism in order to differentiate clearly and avoid getting dragged into competition with the startups and incumbent platforms,

It couldn’t join meetings like Fireflies and Fathom, a lifeless box in Zoom or Meet that feels more like surveillance than productivity. It also couldn’t play favorites with the platforms, working better or worse on Zoom than on Meet.

The former was undoubtedly true, all the way back during the time of investment. The latter was the plan, though initially Granola launched with Google Workspace integration. Chris and Sam always knew that they’d eventually have to launch for Windows, integrate with MSFT products as well as Google, and ultimately be available on both iOS and Android.

The agnostic interface was actually the foundation of the second truth: growth would need to be primarily organic and not paid. To be clear, we were under no illusion that Granola would never pay for new users. However, we (and the Granola team) were adamant that the product would need to create enough user delight, attachment, and emotion to foster an organic viral growth loop.

As very very early users, we immediately recognized the value of the product and the emotional attachment it engendered. The utility piece was obvious – pay attention to meetings during meetings and have easily explorable notes after the fact. But the delight and emotional attachment was surprising.

In retrospect, I’m not sure we fully grasped just how interlinked that user delight was with the foundational platform agnosticism Granola is built upon. I’m not sure that Chris and Sam were aware of it back then either.

Today, it’s very clear. Chris has said to me that Granola feels like a product that is ‘loyal to the user.’ In an environment where the fungibility of software increases every day, a monomaniacal ethos of user alignment becomes a competitive advantage. The program running on your computer is loyal to you first, before your employer, your SaaS stack, FAANG, Big AI, even Granola. That ethos is pushed forward even today with the launch of new APIs.

Each time I start my Granola notes, or hit that lovely “What did I miss?’ button, or search for the context of a meeting that happened twelve months ago, I feel protected and empowered by this product. It’s not about having the answer, it’s about knowing that the answer is safe and available and a click or two away.

The final truth was centered around data. Again, obvious today but less so back then.

The power of LLMs has always been clear to the broader venture ecosystem, including Betaworks. (We had already launched and completed a Camp on LLM-powered cognitive tooling with ThinkCamp prior to the launch of ChatGPT.) But with ChatGPT picking up 100 million users faster than any product in history (by a huge margin), it was clear that the rest of the world was catching up.

The next order effects were becoming clear – context is king. LLMs are only as powerful as the context you can feed them, and feeding them that context was laborious, to say the least.

Conversation data – your words, decisions, priorities, and relationships – is arguably the most valuable unstructured dataset one can leverage as context. Back in 2023, it wasn’t entirely clear to us just how individualized users’ workflows would be. But we knew that whatever team could create stickiness around this dataset would be prepared for whatever the new world required.

It has been a real privilege to work with Chris and Sam and the broader team as they’ve navigated well beyond a simple note-taker to an interface where work gets done. It’s been inspiring to see them build a product that attracts new users and keeps existing ones through gravity – a mutual loyalty – rather than engineered moats and switching costs.

Now, back to meetings. *Enhance notes.*